If you have difficulty paying your bills, it may be worth looking into debt settlement and debt consolidation. Although each method can help you get out debt, they each have their pros and cons. Before you decide which method is best, you need to assess your circumstances.

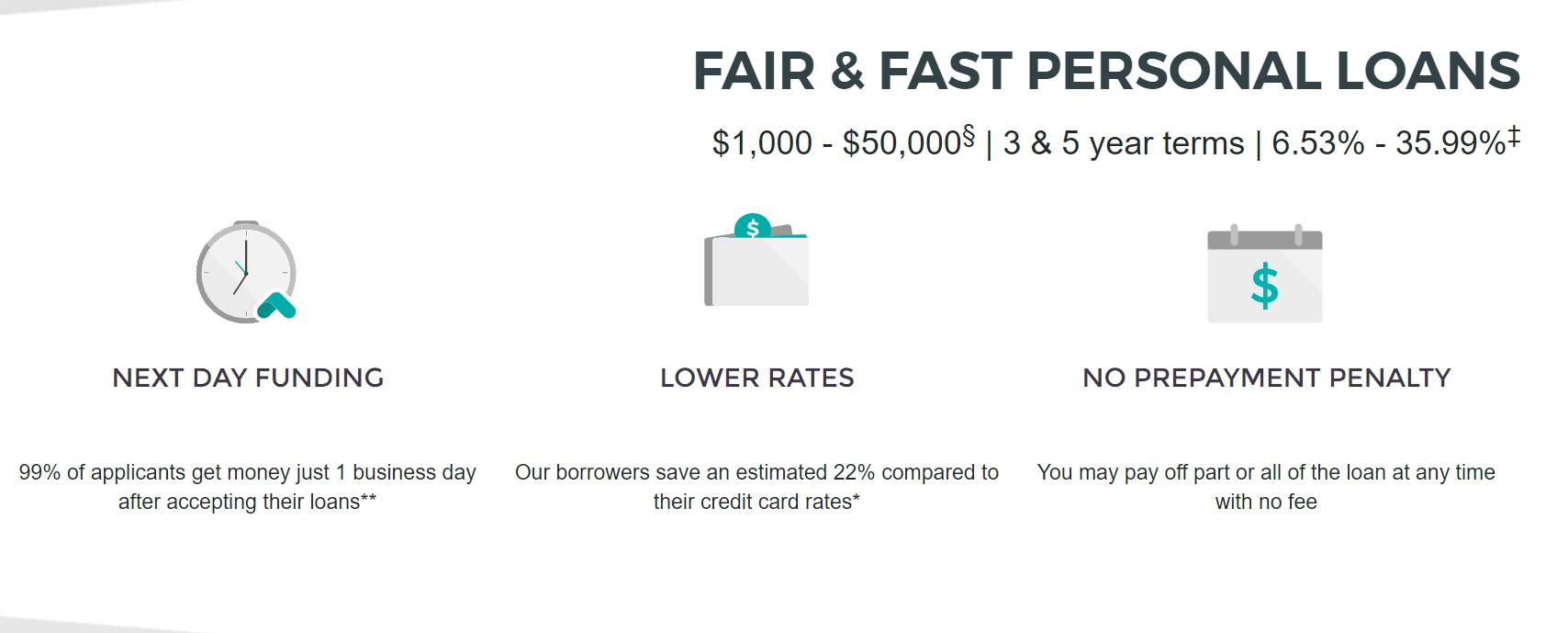

Consolidating debt is the process of consolidating several unsecured loans into one loan, with a lower interest. It can also simplify your finances. To be eligible, however you will need strong credit ratings and income. An experienced debt consolidation firm may charge fees for this service.

The process of settling your debts involves negotiating lower payments with your creditors. This may involve a lump sum payment or a series of payments that can be made over time. In most cases your total payment will not exceed what you owe. Settlement can be used in many cases, including for medical bills and credit cards.

Debt consolidation can be a more effective solution for people who have trouble making their monthly payments. You will see a decrease in interest rates, fees, and you will no longer have to make multiple monthly payments. You'll still need to pay regular monthly payments but will receive a single payment at a lower interest rate.

Debt consolidation has two major disadvantages: higher interest rates, and a negative effect on your credit score. You may see this on your credit history for as long as seven years. A consolidation loan should only be taken out if you have the ability to pay the monthly payments and your income can support your new loan.

If you're considering a debt management plan, you'll need to contact a consumer credit counseling agency. These agencies can help to adjust your budget and create a monthly payment that suits you. You can reduce your monthly payment and stop using credit. This will allow you to avoid additional debt.

Debt settlement is a risky way to deal with your debts, but it can work for you if you're willing to take a hit on your credit report. Debt settlement companies will negotiate with your creditors to lower your interest rates and pay off your debt for less than you owe.

However, debt consolidation won't reduce your total debt. You may still owe more debts than you can repay, even if you consolidate them. Consolidation loans can have higher interest rates than existing loans.

If you are struggling to pay your bills on time or have debts that are too high, debt settlement can be a good option. But it can be risky, and you should only use it if you have no other options available.

Both options can be useful for debt relief. However, you need to consider your financial situation before making a decision about which one is best. You can get free advice and tools from a debt consolidation firm to help you understand this process.

FAQ

What is personal financing?

Personal finance involves managing your money to meet your goals at work or home. This means understanding where your money goes and what you can afford. And, it also requires balancing the needs of your wants against your financial goals.

If you master these skills, you can be financially independent. This means you are no longer dependent on anyone to take care of you. You don't need to worry about monthly rent and utility bills.

It's not enough to learn how money management can help you make more money. It makes you happier overall. When you feel good about your finances, you tend to be less stressed, get promoted faster, and enjoy life more.

What does personal finance matter to you? Everyone does! Personal finance is one of the most popular topics on the Internet today. Google Trends has shown that searches for personal finance have increased 1,600% from 2004 to 2014.

People use their smartphones today to manage their finances, compare prices and build wealth. They read blogs such this one, listen to podcasts about investing, and watch YouTube videos about personal financial planning.

According to Bankrate.com Americans spend on average four hours per day watching TV, listening and playing music, browsing the Internet, reading books, and talking to friends. There are only two hours each day that can be used to do all the important things.

Personal finance is something you can master.

Why is personal finances important?

For anyone to be successful in life, financial management is essential. We live in a world that is fraught with money and often face difficult decisions regarding how we spend our hard-earned money.

So why do we put off saving money? What is the best thing to do with our time and energy?

Yes, and no. Yes because most people feel guilty about saving money. Yes, but the more you make, the more you can invest.

Spending your money wisely will be possible as long as you remain focused on the larger picture.

Controlling your emotions is key to financial success. If you are focusing on the negative aspects of your life, you will not have positive thoughts that can support you.

You may also have unrealistic expectations about how much money you will eventually accumulate. This is because your financial management skills are not up to par.

These skills will prepare you for the next step: budgeting.

Budgeting means putting aside a portion every month for future expenses. You can plan ahead to avoid impulse purchases and have sufficient funds for your bills.

So now that you know how to allocate your resources effectively, you can begin to look forward to a brighter financial future.

What is the fastest way to make money on a side hustle?

You can't just create a product that solves someone's problem to make quick money if you want to really make it happen.

You must also find a way of establishing yourself as an authority in any niche that you choose. This means that you need to build a reputation both online and offline.

Helping other people solve their problems is the best way for a person to earn a good reputation. So you need to ask yourself how you can contribute value to the community.

Once you have answered this question, you will be able immediately to determine which areas are best suited for you. There are countless ways to earn money online, and even though there are plenty of opportunities, they're often very competitive.

You will see two main side hustles if you pay attention. One involves selling products directly to customers and the other is offering consulting services.

Each approach has its pros and cons. Selling products or services offers instant gratification, as once your product is shipped or your service is delivered, you will receive payment immediately.

However, you may not achieve the level of success that you desire unless your time is spent building relationships with potential customers. These gigs are also highly competitive.

Consulting can help you grow your business without having to worry about shipping products and providing services. But, it takes longer to become an expert in your chosen field.

You must learn to identify the right clients in order to be successful at each option. It takes some trial and error. But in the long run, it pays off big time.

How does a rich person make passive income?

If you're trying to create money online, there are two ways to go about it. You can create amazing products and services that people love. This is known as "earning" money.

A second option is to find a way of providing value to others without creating products. This is what we call "passive" or passive income.

Let's suppose you have an app company. Your job is development apps. You decide to make them available for free, instead of selling them to users. That's a great business model because now you don't depend on paying users. Instead, you rely on advertising revenue.

In order to support yourself as you build your company, it may be possible to charge monthly fees.

This is how successful internet entrepreneurs today make their money. Instead of making money, they are focused on providing value to others.

What is the limit of debt?

It is vital to realize that you can never have too much money. You will eventually run out money if you spend more than your income. Because savings take time to grow, it is best to limit your spending. Spend less if you're running low on cash.

But how much is too much? There is no universal number. However, the rule of thumb is that you should live within 10%. Even after years of saving, this will ensure you won't go broke.

This means that if you make $10,000 yearly, you shouldn't spend more than $1,000 monthly. If you make $20,000, you should' t spend more than $2,000 per month. If you earn $50,000, you should not spend more than $5,000 per calendar month.

This is where the key is to pay off all debts as quickly and easily as possible. This includes student loans, credit card debts, car payments, and credit card bill. You'll be able to save more money once these are paid off.

It would be best if you also considered whether or not you want to invest any of your surplus income. If the stock market drops, your money could be lost if you put it towards bonds or stocks. However, if the money is put into savings accounts, it will compound over time.

For example, let's say you set aside $100 weekly for savings. That would amount to $500 over five years. In six years you'd have $1000 saved. You would have $3,000 in your bank account within eight years. It would take you close to $13,000 to save by the time that you reach ten.

You'll have almost $40,000 sitting in your savings account at the end of fifteen years. It's impressive. However, if you had invested that same amount in the stock market during the same period, you'd have earned interest on your money along the way. Instead of $40,000 in savings, you would have more than 57,000.

You need to be able to manage your finances well. If you don't, you could end up with much more money that you had planned.

What is the difference in passive income and active income?

Passive income is when you make money without having to do any work. Active income requires hardwork and effort.

When you make value for others, that is called active income. You earn money when you offer a product or service that someone needs. Examples include creating a website, selling products online and writing an ebook.

Passive income is great because you can focus on other important things while still earning money. Most people don't want to work for themselves. Therefore, they opt to earn passive income by putting their efforts and time into it.

Problem is, passive income won't last forever. If you wait too long before you start to earn passive income, it's possible that you will run out.

In addition to the danger of burnout, if you spend too many hours trying to generate passive income, It's better to get started now than later. If you wait too long to begin building passive income you will likely miss out on potential opportunities to maximize earnings.

There are three types or passive income streams.

-

There are several options available for business owners: you can start a company, buy a franchise and become a freelancer. Or rent out your property.

-

These investments include stocks and bonds as well as mutual funds and ETFs.

-

Real Estate includes flipping houses, purchasing land and renting properties.

Statistics

- These websites say they will pay you up to 92% of the card's value. (nerdwallet.com)

- 4 in 5 Americans (80%) say they put off financial decisions, and 35% of those delaying those decisions say it's because they feel overwhelmed at the thought of them. (nerdwallet.com)

- Shares of Six Flags Entertainment Corp. dove 4.7% in premarket trading Thursday, after the theme park operator reported third-quarter profit and r... (marketwatch.com)

- Etsy boasted about 96 million active buyers and grossed over $13.5 billion in merchandise sales in 2021, according to data from Statista. (nerdwallet.com)

- Mortgage rates hit 7.08%, Freddie Mac says Most Popular (marketwatch.com)

External Links

How To

You can increase cash flow by using passive income ideas

There are ways to make money online without having to do any hard work. Instead, there are passive income options that you can use from home.

There may be an existing business that could use automation. Automating parts of your business workflow could help you save time, increase productivity, and even make it easier to start one.

The more automated your company becomes, the more efficient you will see it become. This allows you more time to grow your business, rather than run it.

A great way to automate tasks is to outsource them. Outsourcing allows your business to be more focused on what is important. You are effectively outsourcing a task and delegating it.

You can concentrate on the most important aspects of your business and let someone else handle the details. Outsourcing can make it easier to grow your company because you won’t have to worry too much about the small things.

Another option is to turn your hobby into a side hustle. It's possible to earn extra cash by using your skills and talents to develop a product or service that is available online.

You might consider writing articles if you are a writer. There are plenty of sites where you can publish your articles. These websites offer a way to make extra money by publishing articles.

Another option is to make videos. Many platforms enable you to upload videos directly onto YouTube or Vimeo. When you upload these videos, you'll get traffic to both your website and social networks.

Investing in stocks and shares is another way to make money. Investing is similar as investing in real property. Instead of renting, you get paid dividends.

They are included in your dividend when shares you buy are purchased. The amount you get depends on how many shares you purchase.

If you sell your shares later, you can reinvest the profits back into buying more shares. You will still receive dividends.